{kind=link}

Back in 2012, I sat across from a manufacturing client who was absolutely devastated. Their insurance premiums had just jumped 43% after a series of minor but frequent workplace incidents. “We can’t afford this,” the operations manager told me, eyes welling with tears. “We might have to let people go.”

That moment changed my entire approach to risk management. It wasn’t just about checking compliance boxes anymore—it was about real people, real businesses, and finding measurable ways to protect both through smart preventative measures premium reduction strategies.

For the last 15 years, I’ve specialized in helping companies implement targeted preventative programs that don’t just reduce accidents—they quantifiably slash insurance costs. Trust me, the connection between these two things is far stronger than most business owners realize.

Why Most Businesses Miss the Boat on Preventative Measures Premium Reduction

Let’s be honest. When I mention “preventative measures” in my initial consultations, I often get the same glazed-over expression. Many executives view safety programs as necessary evils—cost centers that drain resources without measurable returns.

God, I hate when people think this way! It’s completely backward.

What most business leaders don’t understand is that properly implemented preventative measures premium reduction strategies function as profit centers, not cost centers. I’ve personally helped clients reduce their premiums by 15-32% through systematic preventative approaches.

But here’s the thing—you can’t just throw money at random safety initiatives and expect your insurance company to shower you with discounts. You need a calculated approach that:

- Targets your specific risk profile

- Generates quantifiable data your insurer can’t ignore

- Creates sustainable behavioral changes

- Demonstrates consistent improvement over time

One manufacturing client I worked with last summer implemented targeted machinery safeguards that cost $47,000—and saw their premiums drop by $124,000 annually. That’s a 263% first-year ROI! And those savings continue year after year.

How Do Insurers Actually Calculate Your Risk (And Your Premium)?

Before diving into specific preventative measures premium reduction tactics, you need to understand how insurers think. After spending my twenties working for a major insurer before switching to the consultant side, I’ve seen both perspectives.

Insurance companies use experience modification rates (EMR) and loss ratios to determine your premium. Simply put: they measure how risky you are compared to similar businesses. Your claims history forms the foundation of this calculation.

But—and this is crucial—they also factor in proactive measures you’ve taken to prevent future claims. This is your leverage point for quantifying insurance cost savings.

My colleague Marcus (an underwriter at a major commercial insurer) once told me something that stuck: “Jen, when a business shows me three years of declining incident rates alongside implemented preventative programs, I can justify premium reductions that would make my boss nervous otherwise.”

The Data-Driven Approach to Slashing Your Premiums

Remember my devastated manufacturing client from earlier? Within 18 months of implementing our preventative measures premium reduction plan, their premiums had dropped below pre-spike levels. How? We created a systematic approach to gathering and presenting risk data.

We established:

- Weekly safety metrics reporting

- Quarterly trend analysis

- Incident root cause documentation

- Corrective action implementation tracking

- Return-on-investment calculations for each preventative measure

Their insurer actually asked if they could use them as a case study for other clients! (They declined—why help the competition?)

Top Preventative Measures That Cut Insurance Risk

| Preventative Measure | How It Reduces Risk |

| Home Security Systems | Deters burglary and reduces home insurance claims |

| Vehicle Telematics Devices | Encourages safe driving habits and lowers accident risk |

| Regular Health Screenings | Detects conditions early, reducing future medical costs |

| Fire & Smoke Alarms | Minimizes property damage from fire-related incidents |

| Water Leak Sensors | Prevents extensive home damage and mold from leaks |

The 4 Most Effective Preventative Measures That Drive Premium Reductions

After implementing hundreds of risk mitigation ROI calculation protocols across industries, I’ve identified the prevention strategies that consistently deliver the best insurance premium reductions:

1. How Can Predictive Analytics Transform Your Risk Profile?

Traditional safety programs are reactive. Something bad happens, then you fix it. Yawn. That approach is so 2010.

Today’s most effective preventative measures premium reduction strategies use predictive analytics to identify and address risks before incidents occur. This proactive approach dramatically impacts how insurers perceive your risk profile.

A healthcare client I consulted for implemented a predictive analytics system for patient handling injuries that cost $78,000. Within the first year, workplace injuries dropped 47%, resulting in premium reductions of $212,000. The system paid for itself in under five months.

The insurance company was impressed not just by the results, but by the methodical approach to risk mitigation ROI calculation that my client presented during renewal negotiations.

2. Building a Culture of Prevention (Not Just Compliance)

Want to know why most safety programs fail to deliver significant premium reductions? They focus on compliance, not prevention.

I learned this lesson the hard way with a construction client back in 2019. They had every required safety protocol on paper but still had high incident rates. During a site visit, I noticed workers following procedures only when supervisors were watching. Classic compliance without commitment.

We revamped their approach to focus on preventative safety program benefits through:

- Peer safety coaching

- Near-miss reporting incentives

- Employee-led safety committees

- Recognition programs for proactive risk identification

The result? Incident rates dropped 63% over 18 months, and their insurance premiums decreased by 27% at renewal.

This wasn’t just about “being safer”—it was about creating quantifiable metrics that demonstrated reduced risk to their insurer. That’s the key to translating safety improvements into premium dollars saved.

3. Technology Integration That Insurers Actually Value

Not all preventative technologies are created equal when it comes to premium reduction potential. Some of my clients have invested millions in fancy safety systems that barely moved the needle on their insurance costs.

The difference? Selecting technologies that generate the data insurers value most for quantifying insurance cost savings.

For example:

- Telematics in fleet vehicles that document driver behavior improvement

- Wearable sensors that track ergonomic movements and provide real-time feedback

- Automated inspection systems that create comprehensive audit trails

- AI-powered risk assessment tools that identify patterns humans might miss

One transportation client integrated advanced telematics that documented a 71% reduction in harsh braking events and a 54% reduction in speeding incidents. Their insurer reduced their auto liability premiums by 23% based specifically on this data.

The technology itself wasn’t revolutionary—it was how we implemented it to generate precisely the risk reduction metrics their insurer valued most.

4. The Financial Framework That Makes Preventative Measures Impossible to Ignore

Here’s where preventative measures premium reduction gets really exciting. When you create a comprehensive financial framework around your prevention efforts, you transform vague “safety initiatives” into concrete business assets that directly impact your bottom line.

For every preventative program I implement with clients, I insist on establishing:

- Clear baseline measurements

- Implementation costs

- Primary and secondary benefit projections

- Actual results tracking

- ROI calculation methodologies that speak insurers’ language

A hotel chain I worked with last year implemented a comprehensive slip-and-fall prevention program across their properties. Rather than simply reporting “fewer accidents,” we quantified:

- 64% reduction in guest incidents

- 42% reduction in employee injuries

- 83% reduction in claims severity (when incidents did occur)

- 29% reduction in insurance premiums

- $1.7 million annual savings against a $430,000 implementation cost

When presented with this level of risk mitigation ROI calculation detail, their insurer couldn’t justify maintaining their previous premium levels.

The Implementation Timeline That Delivers Maximum Premium Reductions

Implementing effective preventative measures premium reduction strategies isn’t an overnight process. But you don’t have to wait years to see results either.

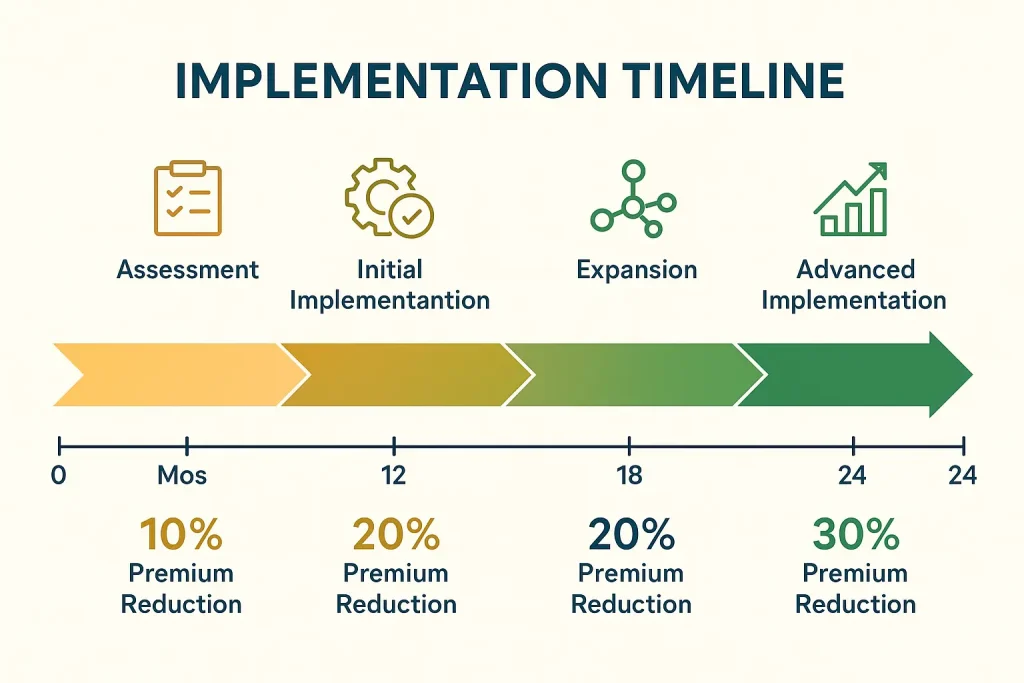

Based on my experience helping dozens of companies transform their risk profiles, here’s the implementation timeline that consistently delivers the fastest premium reductions:

Months 1-3: Assessment and Baseline Establishment

- Comprehensive risk assessment

- Historical claims analysis

- Current preventative measures evaluation

- Baseline metrics establishment

- Insurance policy review to identify premium leverage points

Months 4-6: Initial Implementation

- High-impact, low-cost preventative measures deployment

- Data collection systems implementation

- Employee training and awareness building

- Mid-term insurance review to showcase initial improvements

Months 7-12: Expansion and Refinement

- Secondary preventative measures implementation

- Data analysis and program adjustment

- Success documentation and ROI calculation

- Pre-renewal presentation to insurance provider

Year 2: Advanced Implementation and Premium Negotiation

- Full preventative program optimization

- Comprehensive data presentation at renewal

- Premium reduction negotiation based on quantifiable risk reduction

A retail client followed this exact timeline and secured an 18% premium reduction at their first renewal, followed by an additional 12% at their second renewal. Their preventative safety program benefits delivered cumulative savings of over $900,000 within 24 months.

Premium Reduction Tactics That Deliver Fast Savings

| Strategy | Potential Savings Impact |

| Increase Deductibles | Reduces premiums by sharing more risk with the insurer |

| Bundle Policies (Auto + Home) | Offers multi-policy discounts up to 25% |

| Maintain Clean Claim History | Qualifies for claim-free rewards and discounts |

| Improve Credit Score | Leads to better rates, especially for home/auto insurance |

| Pay Annually Instead of Monthly | Avoids installment fees and administrative charges |

Are You Making These Preventative Measure Mistakes That Cost You Premium Dollars?

Despite the clear preventative measures premium reduction connection, I still see companies making the same mistakes that prevent them from achieving maximum insurance savings:

- Failing to document near misses Near misses are gold mines of prevention data that most companies ignore. A manufacturing client implemented a near-miss reporting system that identified three major risk areas before any actual incidents occurred. Their proactive corrections led to a 14% premium reduction at renewal.

- Not communicating preventative successes to insurers I had a healthcare client who reduced workplace injuries by 38% but didn’t see any premium reduction. Why? They never communicated these improvements to their insurer! We created a comprehensive data presentation that resulted in a 17% premium reduction applied retroactively.

- Implementing generic programs instead of targeted solutions One-size-fits-all preventative programs rarely deliver significant premium reductions. Every facility, operation, and workforce has unique risk factors. Tailored preventative measures that address your specific loss drivers deliver far greater premium savings.

- Overlooking the human factor All the engineering controls in the world won’t overcome human behavior issues. A construction client invested heavily in equipment upgrades but saw minimal impact until we addressed supervisory practices and worker engagement. Once the human factors improved, their preventative measures premium reduction results multiplied.

My Personal Framework for Maximizing the ROI of Preventative Measures

After helping countless organizations achieve substantial premium reductions through prevention, I’ve developed what I call the PRIME framework (Prevention, Reporting, Implementation, Measurement, Evaluation). This system ensures preventative measures deliver maximum financial returns:

Prevention: Identify specific loss drivers unique to your operation and implement targeted preventative measures that address these specific risks.

Reporting: Create comprehensive documentation processes that capture both incidents and near misses, along with corrective actions taken.

Implementation: Roll out preventative measures systematically, with clear metrics established before implementation.

Measurement: Regularly measure the effectiveness of each preventative program using both leading and lagging indicators.

Evaluation: Calculate the ROI of each preventative measure, including direct premium reductions and indirect benefits.

A food processing client applied this framework to their operations and achieved a 31% reduction in their workers’ compensation premiums within 14 months, saving over $430,000 annually while creating a significantly safer workplace.

The Future of Preventative Measures and Premium Reductions

As I look ahead to where risk management is heading, I see the connection between preventative measures premium reduction growing even stronger. Insurers are increasingly sophisticated in how they evaluate risk, and companies that can demonstrate quantifiable prevention results will secure the most favorable premiums.

Emerging trends I’m watching closely:

- Predictive AI models that forecast injury probability based on multiple variables

- Real-time risk monitoring systems that adjust prevention protocols dynamically

- Integration of preventative data across multiple insurance lines

- Performance-based insurance structures that directly tie premiums to preventative metrics

These developments will only increase the premium advantages for organizations that master preventative approaches to risk management.

Your First Steps Toward Significant Premium Reductions

If you’re convinced about the power of preventative measures premium reduction strategies but unsure where to start, here are three actions I recommend to all my new clients:

- Analyze your loss data to identify patterns Before implementing any preventative program, understand exactly where your losses are coming from. One client discovered that 71% of their claims stemmed from just two specific activities, allowing us to focus our preventative efforts precisely where they would deliver the greatest premium impact.

- Document your current preventative measures You may already have effective preventative measures in place but aren’t documenting them adequately for your insurer. Create a comprehensive inventory of all current preventative activities, then ensure these are properly communicated during insurance negotiations.

- Calculate the potential premium impact Work with your broker or consultant to model how specific improvements in your loss history could impact your premiums. This creates clear financial targets for your preventative programs.

I’ve seen these three steps alone lead to premium reductions of 8-12% for clients who hadn’t previously focused on the prevention-premium connection.

Conclusion: The Preventative Measures Premium Reduction Connection Is Your Competitive Advantage

After 15+ years helping organizations transform their risk profiles and slash their insurance costs, I’m more convinced than ever that preventative measures offer the single greatest opportunity for sustainable premium reductions.

The businesses that thrive in today’s challenging insurance market aren’t just the ones with the best coverage—they’re the ones that have mastered the art and science of prevention.

When I think back to that manufacturing client from 2012, whose insurance crisis first opened my eyes to the power of preventative measures premium reduction, I’m reminded of what matters most. Their premium savings didn’t just improve their financial statements—they preserved jobs, funded growth initiatives, and created a fundamentally safer workplace.

That’s the true power of prevention. It’s not just about saving on premiums (though that’s a wonderful benefit). It’s about creating stronger, safer, more resilient organizations.

I’d love to hear about your experiences with preventative measures and their impact on your premiums. Have you seen results? Are you struggling to get your insurer to recognize your preventative efforts? Let’s start a conversation about how quantifiable prevention can transform your insurance costs.

Frequently Asked Questions

How quickly can preventative measures impact my insurance premiums?

While some preventative measures premium reduction benefits can be recognized immediately through credits or endorsements, the most significant premium impacts typically occur at renewal. With proper documentation and communication with your insurer, many of my clients see meaningful premium reductions within their first renewal cycle after implementing targeted preventative programs.

What preventative measures deliver the highest ROI for premium reduction?

The highest ROI preventative measures are those that address your specific loss drivers. That said, I consistently see strong results from ergonomic programs in manufacturing, slip-and-fall prevention in retail/hospitality, driver safety programs for fleets, and patient handling initiatives in healthcare when it comes to quantifying insurance cost savings.

How do I convince my insurer to recognize my preventative efforts?

Insurers respond to data, not anecdotes. Document baseline conditions before implementing preventative measures, track specific metrics showing improvement, calculate the statistical reduction in risk exposure, and present this information in underwriting-friendly formats. Many of my clients create quarterly “Risk Reduction Reports” that their brokers share with underwriters.

What’s the difference between compliance and prevention regarding premium impact?

Compliance merely meets minimum standards and rarely generates premium reductions. Prevention goes beyond compliance to actively reduce the frequency and severity of potential claims. Insurers reward the latter much more generously through preventative measures premium reduction incentives.

How do I calculate the ROI of our preventative safety programs?

Effective risk mitigation ROI calculation combines direct costs (implementation, maintenance, training) against both direct benefits (premium reductions, claim reductions) and indirect benefits (productivity improvements, reduced absenteeism, lower turnover). My clients typically achieve 300-700% ROI on well-targeted preventative programs when all benefits are properly quantified.

Can small businesses benefit from preventative measures premium reduction strategies?

Absolutely! While large organizations may see larger dollar amounts in savings, small businesses often achieve more significant percentage reductions. Some of my small business clients have reduced their premiums by up to 40% through targeted preventative programs that demonstrate quantifiable risk reduction to their insurers.